THE FED JUST GOT A NEW BOSS. HERE’S WHY EVERY DEVELOPER SHOULD CARE.

Kevin Warsh walked into the Federal Reserve on Friday as its new chairman. Jerome Powell walked out — sort of.

Powell, whose term as chair expired, is staying on the Fed’s board of governors. That means Warsh will be voting on rate policy alongside the man he replaced. If you think that dynamic isn’t going to create friction, I have a bridge loan to sell you.

Let’s be honest about what this moment is. It’s historic. It’s messy. And it has direct downstream consequences for every developer financing a deal right now.

The Setup Is Complicated

Trump pushed Powell out in all but name — hammering him publicly for over a year for keeping rates too high. Now he’s installed Warsh, a former Fed governor who served during the Great Recession, with a four-year term as chair and a 14-year seat on the board.

The message from the White House is unmistakable: get rates down.

The problem? The FOMC isn’t listening.

At last month’s meeting, three hawks — Cleveland’s Beth Hammack, Minneapolis’s Neel Kashkari, and Dallas’s Lorie Logan — dissented. Not just on the vote. On the language. They refused to sign off on any wording that implied the next move would be a cut. Their position? A hike might come before a cut does.

That’s not a minor disagreement. That’s a warning shot fired directly at the incoming chair.

Warsh Has One Vote

Here’s the part the headlines bury: Warsh chairs a 12-member committee. He gets one vote. He cannot unilaterally cut rates. He has to persuade a majority — and right now, that majority is leaning the other direction.

Realtor.com senior economist Jake Krimmel put it plainly: practically speaking, convincing this FOMC to cut right now is highly unlikely. They’ve made their views known and put forecasts on the record. And strategically, Krimmel argues, Warsh probably shouldn’t try — because the incoming data, if anything, calls for a hike before a cut.

Read that again. A hike before a cut.

The Data Is Not Developer-Friendly Right Now

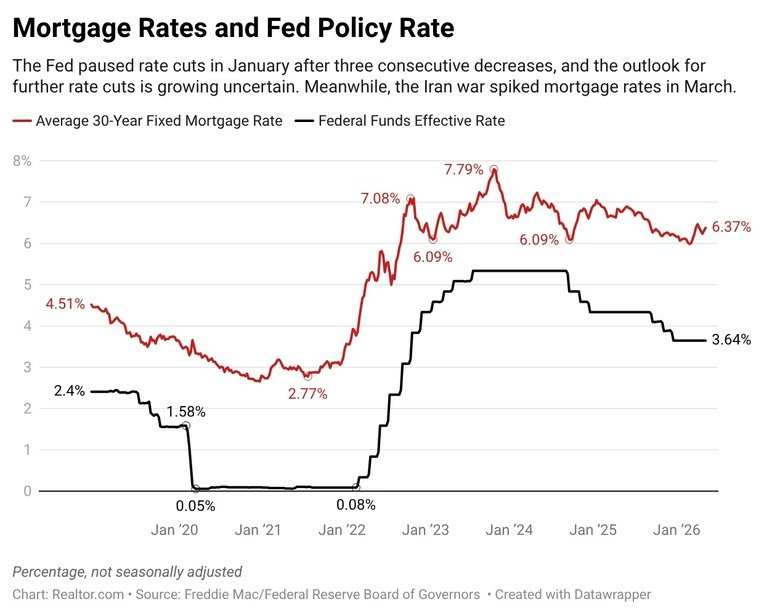

The Fed’s dual mandate is price stability and maximum employment. Right now, both are flashing red in opposite directions — the job market is surprisingly strong while inflation has surged back to a three-year high. That combination historically pushes rates up, not down.

Mortgage rates have already responded. They spiked hard in March after an oil price shock tied to the Iran conflict raised fresh inflation concerns.

For developers relying on construction financing, bridge loans, or rate-sensitive exit strategies, this environment requires discipline. Underwrite conservatively. Don’t model rate relief into your proforma until the data actually supports it.

The Independence Question

This is the part that matters most — not just for markets, but for confidence in the system itself.

Warsh said at his Senate confirmation hearing that Trump never asked him to predetermine any rate decision, and that he’d never agree to do so. That’s the right answer. Whether it’s the true answer is something only time and a genuine economic crisis will reveal.

What’s raised eyebrows is the whiplash: Warsh was a well-known inflation hawk during his 2006–2011 tenure as governor. Then he turned dovish during his job interview for the chairmanship. The timing is, at minimum, awkward.

Krimmel’s assessment: “A chair who is not data-dependent cannot be independent.” The real test won’t come at a routine meeting — it’ll come when Warsh has to make a politically unpopular call. A hike during a Trump administration that wants cheap money. That’s when we’ll find out who Kevin Warsh actually is.

What This Means for Deals

Here’s my developer’s read: don’t bank on lower rates in 2025. The FOMC is skeptical. The data is inflationary. The new chair is untested. And the political pressure — regardless of which direction it ultimately influences policy — creates uncertainty that markets hate.

Uncertainty keeps the risk premium elevated. That means your lenders price wider, your equity partners are more cautious, and your timelines need more buffer.

This isn’t doom and gloom. Deals still get done in high-rate environments. But they get done by operators who plan around reality, not around rate-cut wishful thinking.

Comments

Post a Comment