The Greatest Retail Empire in American History — Built, Neglected, and Looted

How Sears went from selling houses out of a catalog to five stores and a website — and how one hedge fund manager got rich watching it burn.

Part One: The Company That Invented American Shopping

Before Amazon. Before Walmart. Before the mall. There was Sears.

In 1886, a Minnesota railroad station agent named Richard Sears bought a crate of watches a local jeweler didn’t want. He sold them to other station agents along the rail line. That was the spark. He moved to Chicago, hired a watchmaker named Alvah Roebuck, and by 1893 Sears, Roebuck and Company was open for business.

The big idea wasn’t a store. It was a catalog.

In an era when print media reigned supreme, Sears dominated the rural retail market through its massive catalog. Titled the Book of Bargains and later The Great Price Maker, the famous Sears catalog expanded in the 1890s from featuring watches and jewelry to including everything from buggies and bicycles to sporting goods and sewing machines. It educated millions of shoppers about mail-order procedures, and used simple, informal language with a warm, welcoming tone.

Rural America had no access to urban department stores. Sears brought the store to them — by mail. “We solicit honest criticism more than orders,” the 1908 catalog stated. Sears didn’t just sell goods. Sears taught Americans how to shop.

Then came the cars. And with cars came suburbs. And Sears adapted.

In 1924, Sears hired Robert Ward — “the General” — who drove the company’s growth over the next 30 years. One of his main innovations was opening physical stores where customers could buy goods directly rather than wait for the post office.  The first store opened in Chicago in 1925, and the number grew so rapidly that by 1931 retail sales had topped mail-order sales.

That pivot — catalog to stores, rural to suburban — was the first great reinvention. It would not be the last.

By the post-war boom, Sears was the beating heart of the American middle class. You bought your refrigerator there. Your tools. Your tires. Your insurance. Your credit card. The company expanded aggressively into suburban shopping malls, capitalizing on the automobile boom. During this period, Sears introduced several private-label brands — Craftsman, Kenmore, and DieHard — which became synonymous with quality and fostered fierce customer loyalty.

Let’s talk about those brands, because they deserve their own paragraph.

Craftsman. Sears paid $500 for the rights to the Craftsman brand in 1927. The brand became known for high-quality tools with a lifetime guarantee. Craftsman later branched out into lawnmowers, power tools, and even electric razors to serve a growing suburban base.

Kenmore. Sears introduced the first Kenmore washing machine in 1927 and the first Kenmore vacuum cleaner in 1932. Throughout the 1970s, Sears continued to expand the Kenmore brand across refrigerators, freezers, and air conditioners.  Kenmore didn’t just sell appliances. It changed family life.

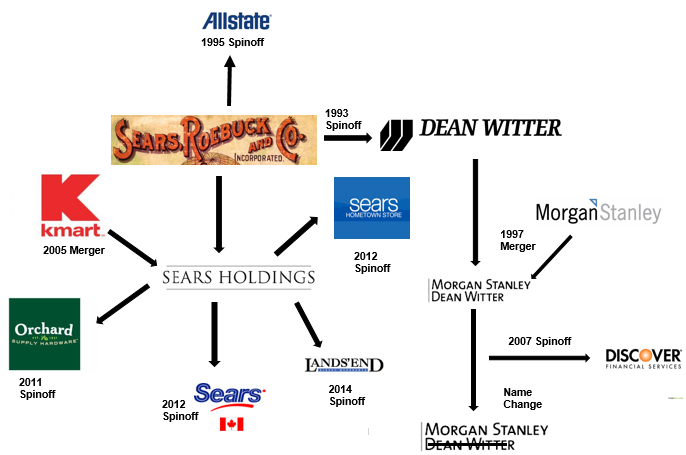

Allstate. Sears offered car insurance for the first time, borrowing the name from a set of tires sold in the catalog. Sears retained complete ownership of Allstate until 1993, when it sold a 20% stake in what was the nation’s biggest IPO at the time.

Discover Card. In 1985, Sears introduced the Discover Card — the first to offer cash rewards to customers based on spending. It was wildly popular. Within four years, 20 million people had the card.

And then — because they literally ran out of ambitions at street level — they built up.

Sears announced plans to build a new headquarters in downtown Chicago in 1969. At the time, Sears was the largest retailer in the world with approximately 350,000 employees. When it opened in 1973, the 110-story Sears Tower dominated the Chicago skyline as the tallest building in the world — a distinction it held for 25 years.

The tallest building on Earth. Built by a company that started selling watches out of a railroad station.

Between 1906 and 1972, Sears’ stock market capitalization increased over 1,200-fold — from $15 million to $18 billion. After reinvesting dividends, $1 invested in Sears in 1908 grew to over $20,000 by 1972, making Sears one of the greatest investments in American history.

That was the peak.

Part Two: The Slow Fade — How Sears Forgot to Reinvent Itself

Success makes companies lazy. Sears was no exception.

The same adaptability that built Sears into a giant in 1925 — the willingness to blow up the catalog model and build stores — went missing by the 1970s. New competitors arrived. Sears didn’t take them seriously.

In 1962, Target, Walmart, and Kmart were all founded — three companies that would eventually replace Sears in the retail market. In the 1970s, high inflation pushed lower-income consumers to discount retailers, while higher-end customers gravitated toward more fashionable stores.

Sears was stuck in the middle. Too expensive for bargain hunters. Too boring for aspirational shoppers.

In 1967, Sears posted $1 billion in monthly sales for the first time. Construction began in 1970 on the 110-story Sears Tower. That era was fading, however, even as its monument rose above the Chicago skyline.

The irony is almost too perfect. They were literally building a monument to themselves at the exact moment the slide began.

In the 1980s, Sears expanded by buying Dean Witter and Coldwell Banker and introducing the Discover Card. But these businesses weren’t central to their traditional operations, and the company was forced to change course. By the end of the decade and into the 1990s, Sears had sold the Sears Tower, most of the non-retail lines, and ceased their long-running catalog.

The catalog. Gone in 1993. The thing that built the empire, discontinued. Not replaced by e-commerce. Just… ended.

In 1991, Walmart overtook Sears as the nation’s largest retailer. Sears took many different tacks under a series of problematic leaders, losing sight of its traditional niche, which it ceded to discounters. Its credit card business, for example, accounted for 60 percent of its profits at the turn of the 21st century.  A retailer surviving on interest income. Not a good sign.

By 2003, even that was gone — Sears sold its credit and financial business to Citigroup for $32 billion. But by then, Walmart, Target, and Home Depot all had greater sales than Sears.

Sears was the retailer people used to go to, not the one they went to. Sears was no longer innovating and showing other retail stores how they needed to change.

That’s the brutal truth. Sears didn’t get disrupted overnight. They had decades of warning. They watched Walmart, Target, and Home Depot eat their lunch — one category at a time — and never landed a counterpunch.

Then came the man who would finish the job.

Part Three: Eddie Lampert and the Looting of a Legend

In 2003, a hedge fund manager named Eddie Lampert bought the debt of bankrupt Kmart and seized control of the company. Pundits called him the “Steve Jobs of the investment world.” The new Warren Buffett. By 2006 he was the richest man in Connecticut, managing over $15 billion through his hedge fund, ESL Investments.

In 2005, Lampert bought control of Sears for $11 billion, having already built up a 15% stake. As part of the deal, Sears merged with Kmart, which Lampert had bought out of bankruptcy two years earlier.

Wall Street loved it. The retail world was skeptical. The skeptics were right.

Lampert had no retail experience. What he had was an ideology and a spreadsheet. An outspoken advocate of free-market economics and fan of Ayn Rand, he restructured Sears so that each business unit functioned like an autonomous company with its own president, board of directors, and profit-and-loss statement. He expected the invisible hand of the market to drive better results.

The theory: competition would make each unit sharper, leaner, better. The reality was a corporate Hunger Games.

He radically restructured operations, splitting the company into thirty — and later forty — different units that were to compete against each other. Instead of cooperating, divisions like apparel, tools, appliances, human resources, IT, and branding were to operate as autonomous businesses, each with their own president, board of directors, and profit-and-loss statement. One former executive described a culture of “warring tribes” and the elimination of cooperation and collaboration.

The apparel division cut back on labor to save money, knowing that floor salespeople in other departments would pick up the slack. Turf wars sprang up over store displays. No one was willing to make sacrifices in pricing to boost store traffic.  Lampert eventually instituted a bidding system, forcing units to pay for advertising space in the company circular. The wealthier divisions — like appliances — could buy more. For the 2011 Mother’s Day circular, the sporting-goods unit purchased cover space for a children’s minibike.

Meanwhile, the stores rotted. The lack of investment in Sears and Kmart stores turned them into barren, outdated relics.  While Amazon was building the future of retail and Target was renovating for a modern shopper, Sears locations were collapsing into themselves.

But here’s where the story gets darker. Because Lampert wasn’t just failing at retail. He was succeeding at something else entirely.

The Real Estate Play

In 2015, Lampert split off 235 of Sears’s most profitable stores and 31 other real-estate holdings, selling them to a publicly traded REIT called Seritage Growth Properties for $2.7 billion. The sale/leaseback deal had Sears paying Seritage rent on facilities it once owned. Lampert’s hedge fund owned 43.5 percent of the Seritage limited partnership, and he served as its chairman.

He was on both sides of every deal. Deciding which stores to close. Collecting the rent. Pocketing the termination fees.

He also faced scrutiny for loading up Sears Holdings with debt from his own hedge fund.  From 2016 to 2018, Sears Holdings paid more than $400 million in “interest” and “fees” on loans made by Lampert, his affiliates, and others.  The patient was hemorrhaging cash. The doctor owned the blood bank.

The brands went next. Sears sold the Craftsman brand to Stanley Black & Decker in a deal valued at $900 million. While Sears got the cash it needed, it lost its ability to sell the still popular brand exclusively.  He also sold the DieHard automotive battery brand, leaving Kenmore as the lone survivor in the portfolio.

Lands’ End was transferred to Lampert’s hedge fund ESL Investments at a time when it had an enterprise value of $1.3 billion.

The Lawsuit

After the bankruptcy filing in October 2018, creditors came looking for their money.

Sears Holdings sued Lampert, alleging the billionaire stripped the company of more than $2 billion in assets. “Altogether, Lampert caused more than $2 billion of assets to be transferred to himself and Sears’ other shareholders and beyond the reach of Sears’ creditors,” the suit stated.

The suit cited an email from former Sears Holdings CFO Robert Schriesheim attempting to explain the Lands’ End deal: “[Lampert] was trying to optimize cash for [Sears] while maximizing his [ESL Investments] equity stake… because he knows that [Lands’ End] is worth a great deal outside of [Sears].”

The settlement reached in 2022 was $175 million  — a fraction of what was alleged to have been extracted. Lampert called the claims baseless. The creditors called it a start.

The Aftermath: Five Stores and a Website

From 2,705 stores at its peak in 2011, only five stores are still open in the U.S. as of December 2025.

Five stores. From the tallest building in the world to a handful of struggling locations and a website that looks like it was designed during the Bush administration.

The brands Sears invented — Craftsman, Allstate, Discover, DieHard — are now worth billions under other owners. The real estate that Sears sat on for decades is being redeveloped into apartments, offices, and mixed-use commercial projects. Seritage has used the real estate from closed Sears locations to sign new tenants at much higher rents or to redevelop properties into commercial developments such as apartments and offices.

The land won. The store lost.

What This Tells Us About Retail — and About People

The Sears story has two lessons that cut in opposite directions.

Lesson one: Companies that refuse to change die. Sears saw Walmart coming in 1962. They watched Amazon emerge in the late 1990s. They had decades of warning and spent it diversifying into financial services, building bigger headquarters, and hoping the problem would go away. It didn’t.

Lesson two: Capital without operational competence is destruction dressed up as strategy. Lampert wasn’t bad at running Sears because he was incompetent. He was bad at running Sears because he was never really trying to run Sears. He was running a liquidation event — with himself on both sides of every transaction.

The stores that Sears built, the brands it created, the real estate it accumulated — all of that value was real. It didn’t evaporate. It was extracted. Methodically. Legally. Profitably. For one man.

Richard Sears started a business selling watches out of a railroad station because he saw an opportunity to give ordinary Americans access to things they couldn’t otherwise afford.

Eddie Lampert bought that business 130 years later, and gave ordinary Americans one last thing they couldn’t afford: a place to shop.

Daniel Kaufman is a real estate developer and investor based in California and Maine, focused on affordable and workforce housing development across the country. He writes about real estate, capital markets, and the stories hiding inside American business history.

Comments

Post a Comment