Raw Land Up 87% Since 2019. The Correction Is Here. Here’s What It Means for Developers.

Let me give you the number that should have every land-hungry developer paying attention: raw land prices surged 86.5% between early 2019 and March 2026. Not build-ready lots. Not partially improved parcels. Raw dirt. The stuff with no utilities, no clearing, no entitlements — just acreage and a dream.

According to Realtor.com’s first-ever land listing analysis, overall land prices per acre climbed roughly 77% over that same stretch, while inventory of for-sale parcels cratered 24%. The pandemic lit a fire under a market that was already supply-constrained, and developers — chasing historically cheap debt — ran hard at every acre they could find.

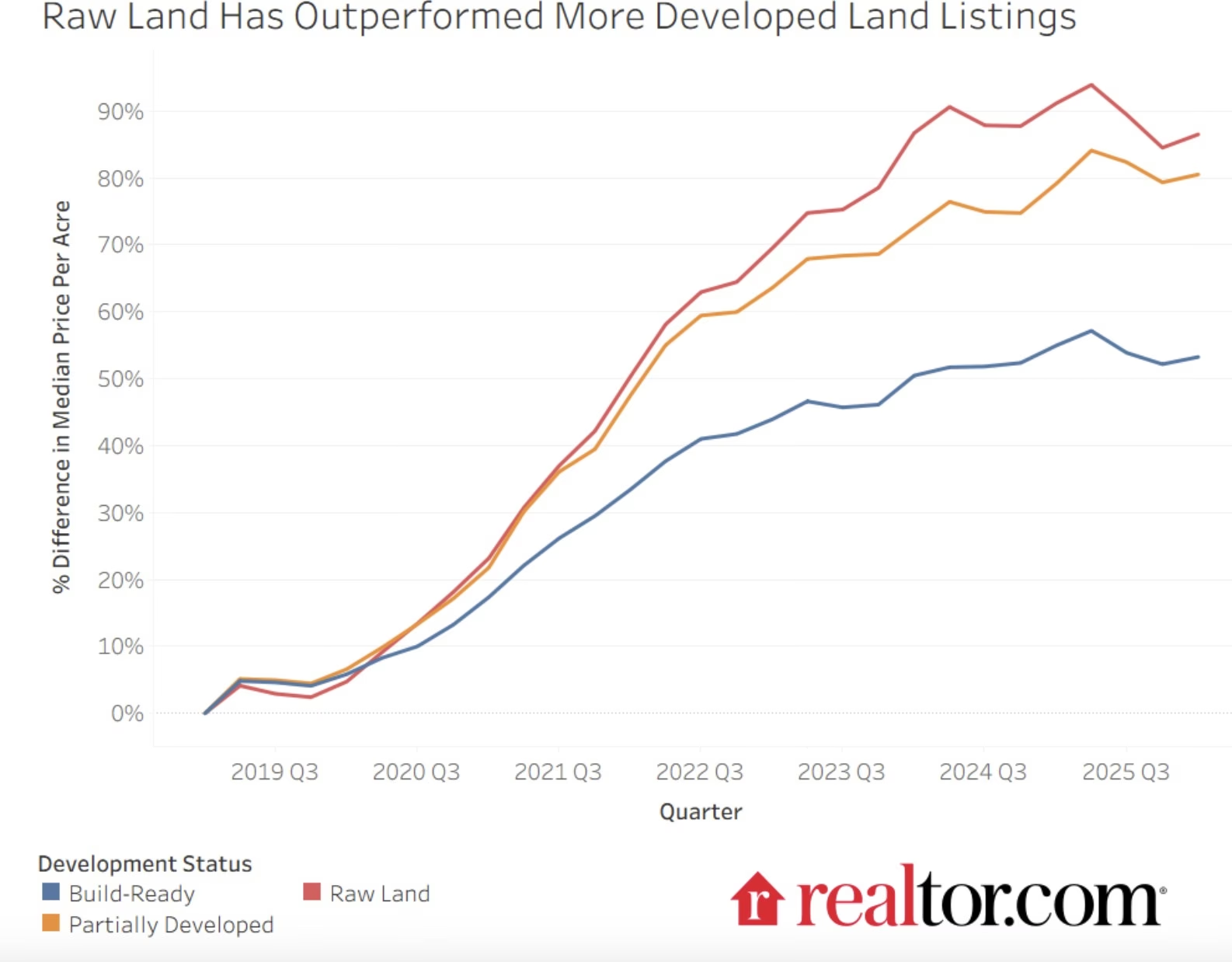

The result? A tiered appreciation story.

• Raw land: +86.5%

• Semideveloped parcels: +80%

• Build-ready lots: +53.3%

Why did raw land outrun everything else? Two reasons, according to Realtor.com senior economist Joel Berner. First, it started from a lower price point — more room to run. Second, build-ready lots have a natural ceiling baked in: they can only be worth so much before the math on the home you’d build stops working. Raw land has no such ceiling. It trades on speculation and vision, not comps.

That’s exactly right. And as someone who acquires land for development, I’d add a third factor nobody talks about enough: raw land is where developers compete before the game is over. By the time a parcel is build-ready, the hard work — entitlements, infrastructure, environmental review — is already priced in. The margin is gone. Raw land is where you find the spread.

The Correction Has Started — and That’s Good News

Here’s what’s changed: the frenzy is over. Land prices have begun to soften.

Overall land values dropped 0.5% from early 2025 to early 2026. Raw land led the correction with a 2.4% year-over-year price decline. Build-ready lots fell 1.1%. Semideveloped parcels were the one exception, ticking up 0.8%.

The culprit is no mystery. New residential construction finished 2025 below 2024 levels. Builders are pulling back. Homebuyer demand is soft. When builders stop acquiring land, land prices fall. Simple as that.

For patient, well-capitalized developers who didn’t overpay at the peak? This is the window. Motivated sellers, reset prices, and less competition from spec buyers who are now underwater on their 2021-2022 land bets.

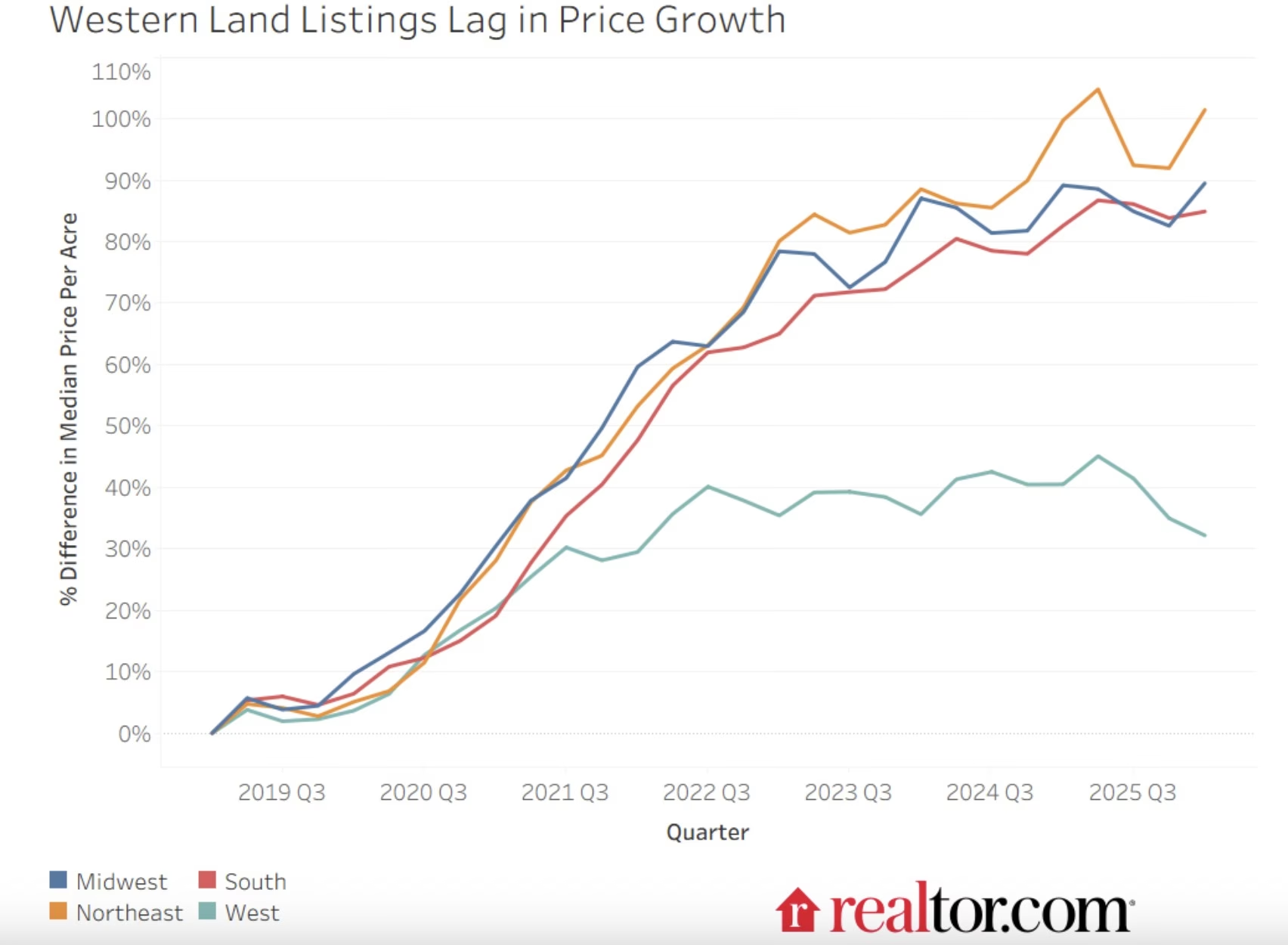

Geography Matters: The Northeast Won, the West Got Left Behind

Here’s the regional breakdown since 2019:

• Northeast: +101.4%

• Midwest: +89.5%

• South: +84.9%

• West: +32.1%

The Northeast’s extreme scarcity of buildable land — it had the fewest listings before the pandemic — meant that any incremental demand compression sent prices vertical. The supply was already tight. It got tighter. Prices responded accordingly.

The West tells the opposite story. In a place like Teton County, Wyoming, less than 3% of the land base is privately held. There’s almost nothing to trade. Environmental review alone can add years to a project. Fire risk assessments, water rights, access easements, utility extensions — the carrying cost and timeline risk in premier Western markets is brutal. Builders followed the path of least resistance east, where supply is deeper, entitlement is faster, and margins are more predictable.

The result: Western land prices dropped 5.9% over the past year alone — the steepest regional pullback in the country — as builder demand retreated and housing inventory in several Western states returned to or exceeded pre-pandemic levels.

The Takeaway for Developers

If you’re acquiring land right now, here’s how I read this data:

The speculative premium is deflating. Raw land that got bid up on pure optionality — no entitlements, no path to approval, just hope — is correcting hardest. Good. That’s capital misallocation unwinding.

The Northeast and Midwest are still structurally undersupplied. Prices have moderated, but the underlying scarcity hasn’t changed. Those markets reward patient, disciplined buyers.

Raw land still beats build-ready for developers who can do the work. The spread is in the entitlement process. If you can take a raw parcel through permitting and infrastructure installation, you’re creating value. That’s the job. The correction just made the entry point better.

The land market spent four years pricing in a future that may not arrive on the original timeline. Now it’s recalibrating. For developers who know what they’re doing, that’s not a problem.

That’s an opportunity.

— Daniel Kaufman | danielkaufmanrealestatedeveloper.blogspot.com

Daniel Kaufman is a real estate developer and investor based in Maine, with an active portfolio spanning affordable housing, workforce housing, and mixed-use development across New England and beyond. His current projects include Sunridge on Searles, a modular tiny-home community in Las Vegas, and pre-development work across five New England markets. Daniel writes about land, capital, development economics, and the forces reshaping where, and how, Americans live. He is an avid skier, a Sunday River season pass holder, and a firm believer that the best deals are made before the dirt gets entitled.

Follow him on Instagram at @DanielKDevelops

Comments

Post a Comment