America’s Housing Shortage Is Still Getting Worse

A new report confirms something those of us working in housing already know firsthand: the United States simply isn’t building enough homes. Not for renters. Not for first-time buyers. And especially not for lower-income households.

According to the National Low Income Housing Coalition’s latest annual report, the country is short 7.2 million affordable and available rental homes for very-low-income renters—those earning less than 30% of their area’s median income. For every 100 households in that income bracket, there are only 35 affordable units available.

That shortage forces millions of families into impossible tradeoffs. Many become severely cost-burdened, spending such a large share of their income on rent that saving for homeownership—or even financial stability—becomes unrealistic.

But the shortage doesn’t stop there. It’s part of a much larger structural problem in the housing market.

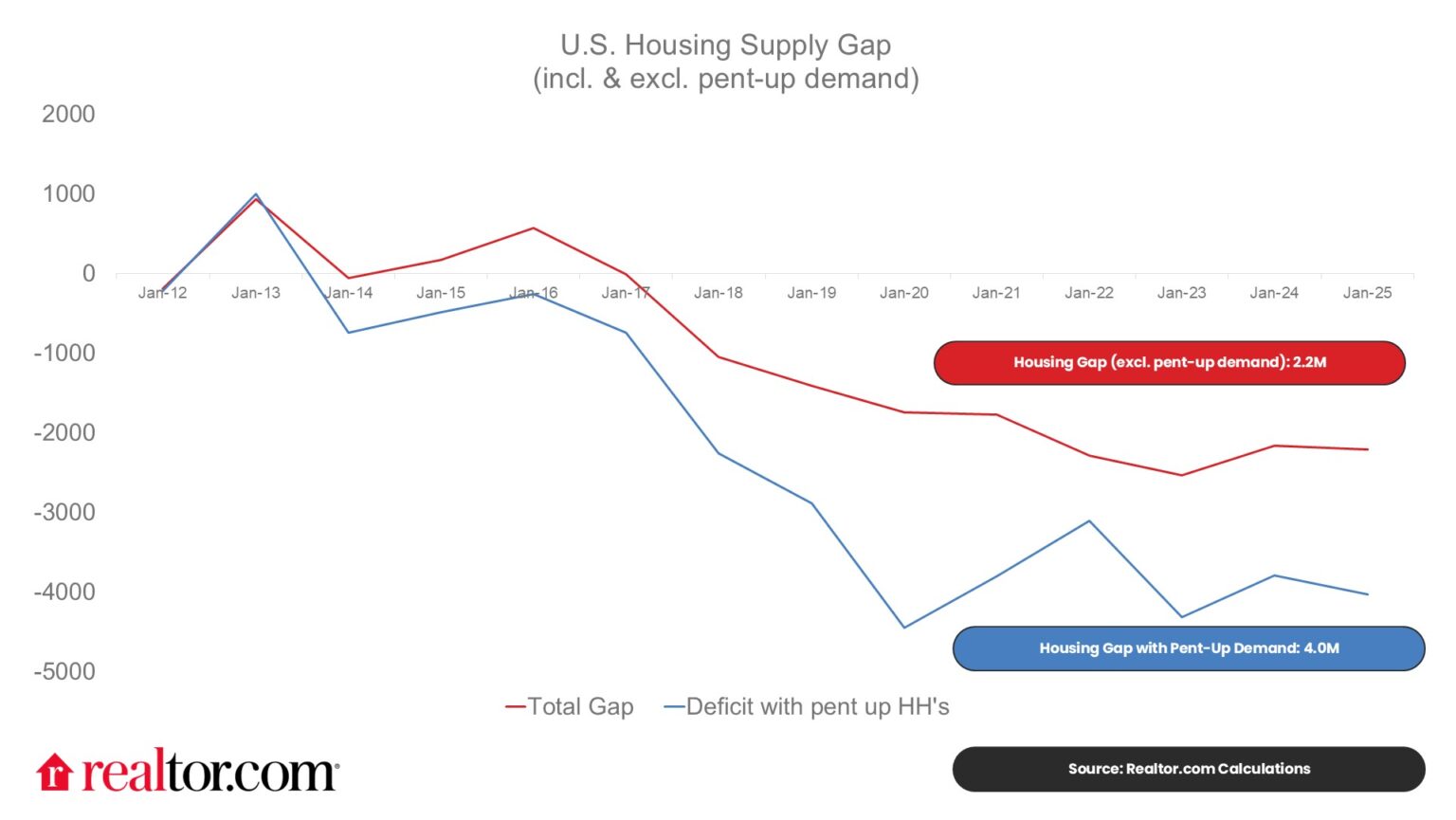

The National Housing Gap Has Surpassed 4 Million Homes

Separate research from Realtor.com estimates the overall U.S. housing shortage at 4.03 million homes.

Even in years when construction appears relatively strong, the math simply doesn’t work. In 2025:

- About 1.4 million households were formed

- Only 1.36 million homes were started

That gap might seem small on an annual basis, but the cumulative shortage keeps growing because the deficit from the past decade was never resolved.

Since the early 2010s, the United States has underbuilt housing for more than a decade. The result is a structural imbalance that continues to push prices higher and keep ownership out of reach for younger households.

Millions of “Missing” Households

One of the most striking findings is how many potential households never formed at all because housing became too expensive.

Researchers estimate that 1.82 million Gen Z and millennial households were “missing” in 2025.

Instead of forming their own households, many young adults are:

- Living with parents

- Sharing housing with roommates

- Delaying family formation

- Postponing homeownership

The numbers tell the story. The median age of a first-time homebuyer hit 40 in 2025, the highest ever recorded.

Meanwhile, the income needed to buy a median starter home is roughly $86,000, and the typical down payment now exceeds $30,000. At current savings rates, the median household would need about seven years just to accumulate that down payment.

The Affordable Housing Crisis at the Bottom of the Market

While the broader housing shortage affects everyone, it’s most severe for the lowest-income households.

Very-low-income renters—those earning under 30% of area median income—are a diverse group:

- Roughly one-third are working in low-wage jobs

- Another third are seniors

- About 18% have disabilities

- A smaller share are students or caregivers

For these households, market-rate construction alone rarely produces housing they can afford. That’s why many experts argue that subsidized housing programs are still necessary.

Programs like the Low Income Housing Tax Credit (LIHTC) remain one of the primary tools for financing affordable housing developments in the U.S.

Why Supply Still Matters

Even though affordable housing often requires subsidies, increasing overall supply still plays a critical role.

When new housing is built:

- Higher-income renters move into new units

- Older units become available at lower price points

- Pressure on rents eases across the market

Economists often call this a filtering effect, and it’s one reason many policymakers are now focused on reducing zoning barriers and permitting delays.

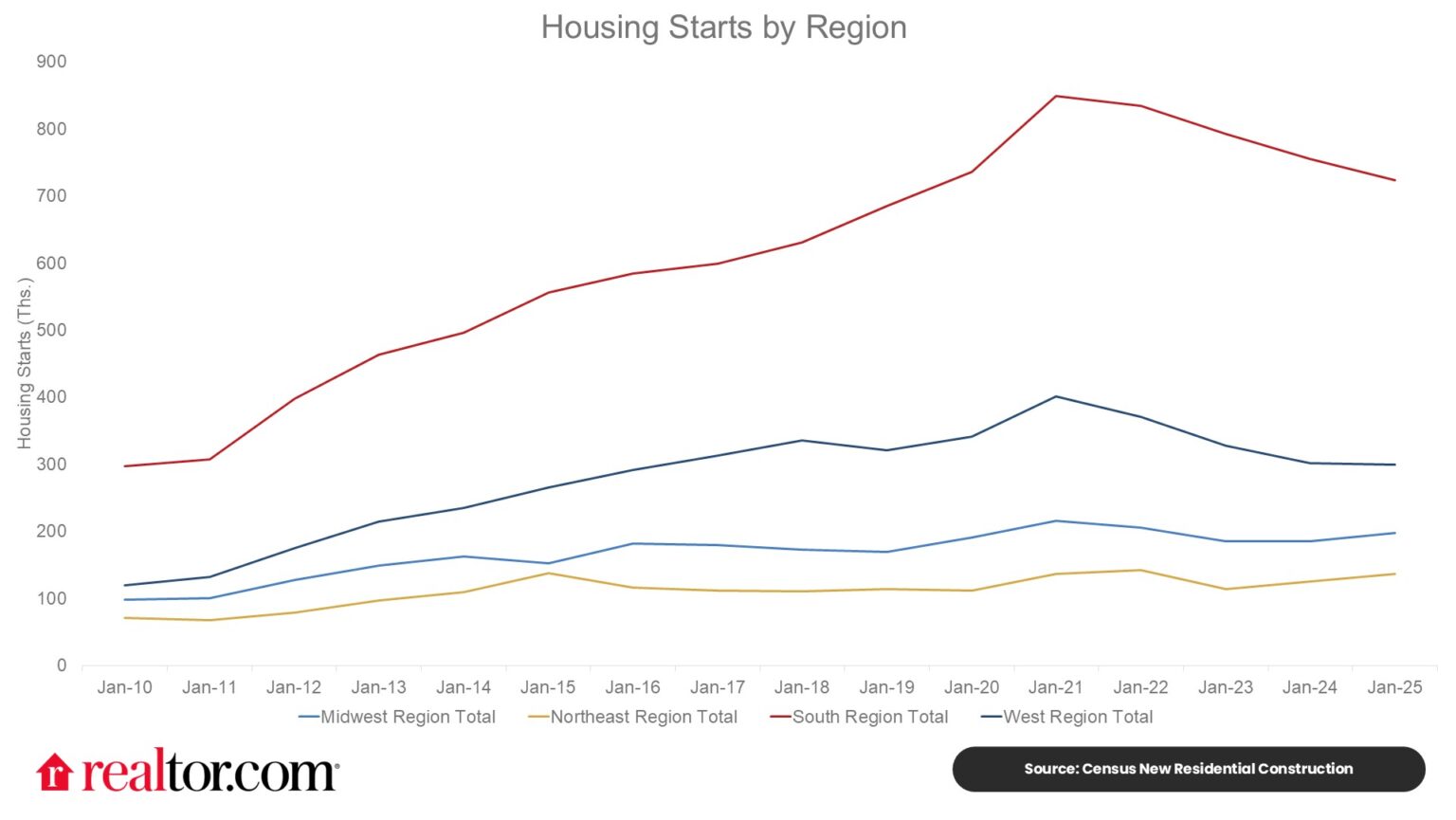

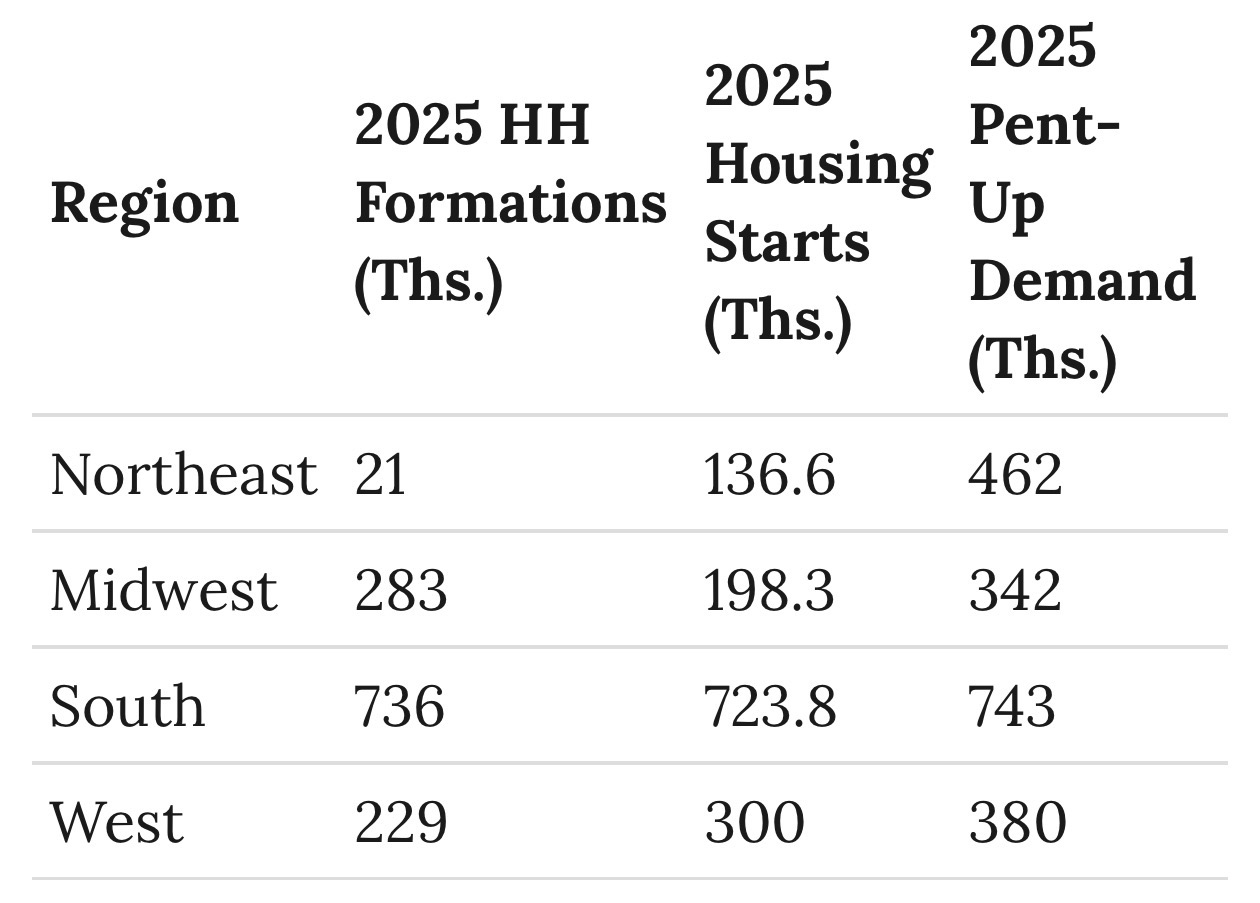

Regional Differences in the Housing Shortage

The housing deficit varies widely across the country.

- South: Largest shortage in absolute terms (about 1.62 million homes)

- Northeast: Most severe shortage relative to construction history

- Midwest: Growing shortage as affordability attracts migration

- West: Smaller relative gap but still constrained in many major metros

Interestingly, the Northeast was the only region where the supply gap slightly improved in 2025, largely because construction reached its highest levels in a decade.

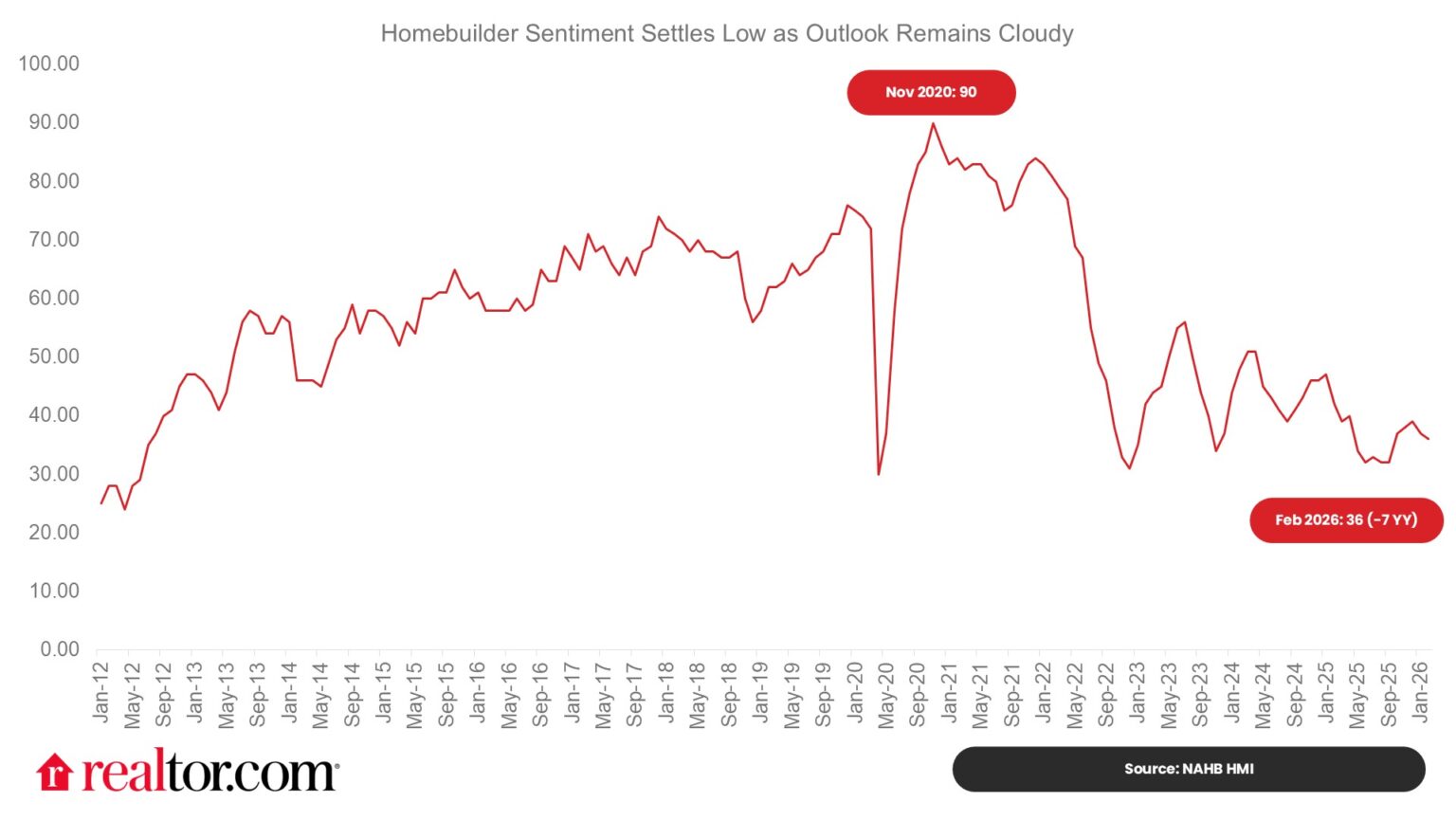

Builders Are Facing Their Own Challenges

Developers are often blamed for the housing shortage, but the reality is more complicated.

Builders today face a combination of headwinds:

- Zoning and permitting restrictions

- Labor shortages in the construction industry

- Higher material costs

- Tariffs on building inputs

- Uncertainty about buyer demand

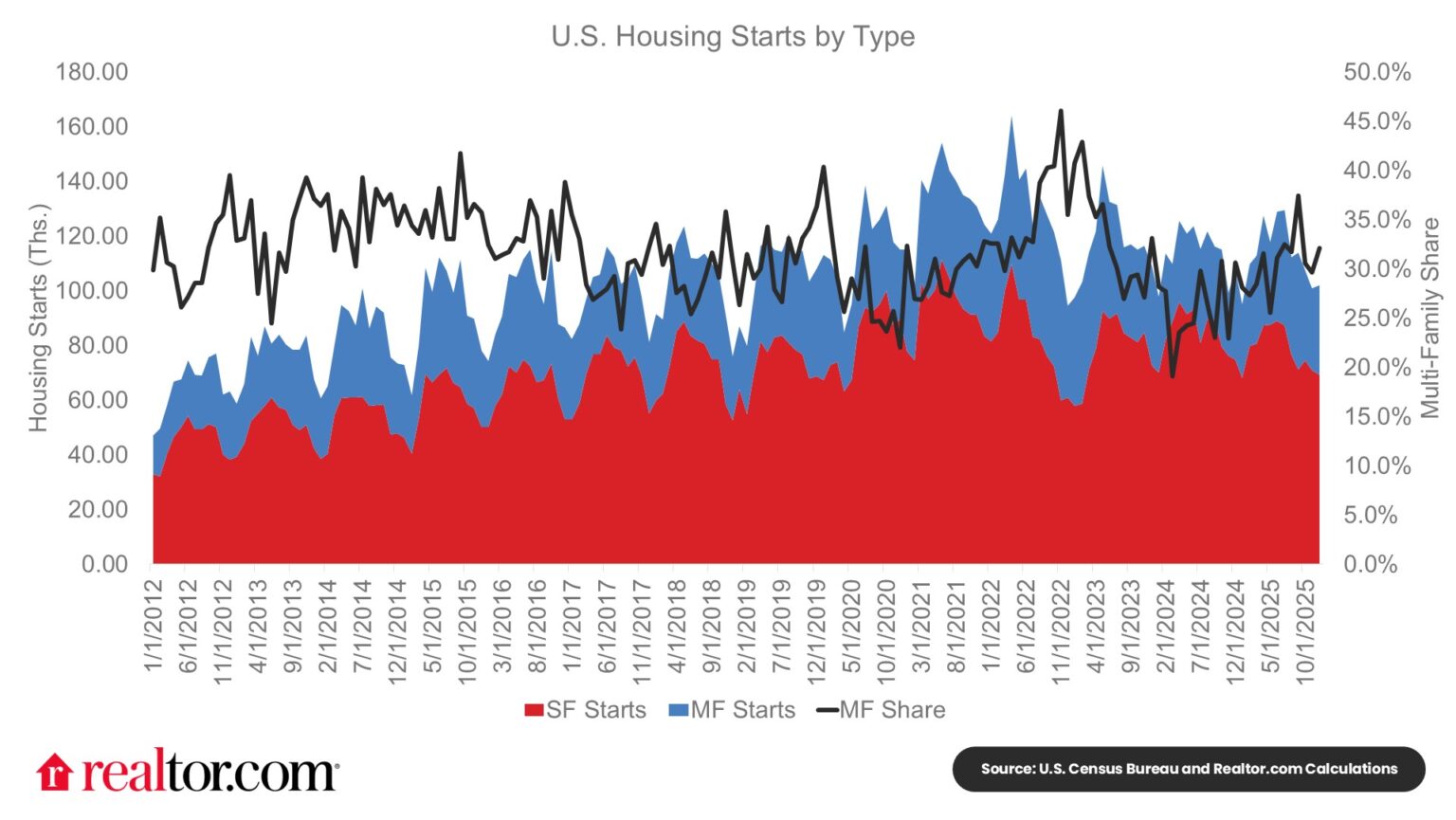

These pressures contributed to the lowest level of single-family housing starts since 2019.

Even so, new construction continues to play an outsized role in the market. Nearly 15% of all homes sold in 2025 were newly built, the highest share since 2005.

Closing the Gap Will Take Years

Even under optimistic assumptions—such as increasing construction by 50% above current levels—economists estimate it would take roughly seven years to eliminate today’s housing deficit.

And that assumes pent-up demand disappears, which is unlikely.

What this means in practice is that housing policy needs to focus on both supply and affordability simultaneously.

More homes must be built. But they also need to be built in the right places—near jobs, infrastructure, and growing populations.

The Bottom Line

Housing has always been more than just shelter. It’s the foundation for financial stability, family formation, and long-term wealth creation.

Right now, millions of Americans are locked out of that pathway.

Until the United States dramatically increases housing production—while also expanding tools that support affordability—the housing shortage will remain one of the defining economic challenges of the next decade.

Comments

Post a Comment